CBRE notes that capitalization rates (cap rates) were broadly stable in the second half of 2019 and relatively stable for full-year 2019 in its recently published survey for income producing commercial real estate (retail, office, industrial, multifamily and hotel) as of December 31, 2019.

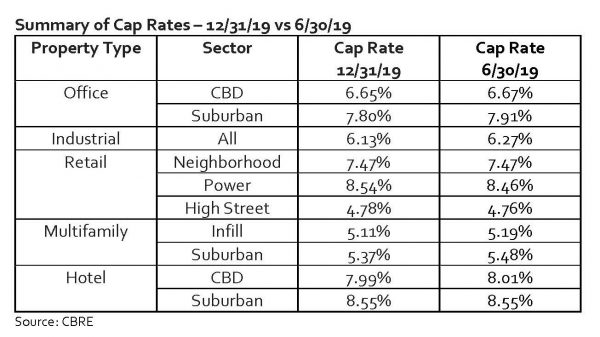

Within the retail sector, CBRE noted that tertiary markets and Class C properties attracted increased investment activity among private buyers due to higher risk tolerance and opportunities for redevelopment. Grocery-anchored neighborhood/community centers remained the favorite retail asset class because of perceived resilience to e-commerce. Retail cap rates for neighborhood and community shopping centers were unchanged, while cap rates for power centers edged up 8 basis points (bp) and high-street retail declined 2 bp. Recent store closures and bankruptcies are negatively impacting retail sentiment, particularly in the power center segment

Suburban multifamily cap rates tightened most across lower-quality properties and declined 11 bp overall. Cap rates between Class A and Class C assets and primary versus tertiary markets continued to tighten, indicating better opportunities in lower quality assets and smaller markets. Infill multifamily cap rates decreased 9 bp. Industrial cap rates also compressed 13 bp, on top of a 5 bp decline in the first half of 2019. Office cap rates compressed 11 bp. Hotel cap rates were unchanged.

CBRE projects continued cap rate stability for the first half of 2020 across property types, segments, and market tiers, except for a slight increase in the hotel sector.